Our Expertise

Looking to grow your real estate portfolio without the hassle of income verification or tax returns? Our investment property loans powered by DSCR (Debt Service Coverage Ratio) financing are designed specifically for real estate investors like you—focused on property income, not personal income.

Tailored Solutions

Empowering Your Financial Journey

What is a DSCR Loan?

A DSCR loan (Debt Service Coverage Ratio loan) is a type of investment property loan that qualifies you based on the cash flow of the rental property—not your W-2s, pay stubs, or tax returns.

Instead of verifying your personal income, lenders calculate the property's rental income divided by its monthly debt obligations (loan payment, taxes, insurance, etc.). This ratio determines if the property can cover its own expenses.

Benefits of DSCR Investment Property Loans

✓ No Personal Income Documentation

Skip the tax returns, W-2s, or pay stubs. Approval is based on property income.

✓ Fast Closings

With fewer documents required, DSCR loans often close faster than conventional loans.

✓ Perfect for Investors

Ideal for borrowers with multiple properties, self-employed investors, or those using Airbnb/short-term rental income. Canadian investors welcome.

✓ Flexible Property Types

Finance single-family homes, condos, townhomes, 2–30 unit properties, and even short-term rentals.

✓ Refinance & Cash-Out Options

Use DSCR loans to purchase, refinance, or pull equity from existing investment properties.

How DSCR Loans Work

When you apply for a DSCR investment property loan, the lender evaluates:

Gross Monthly Rent (from a lease agreement or appraiser’s market rent estimate)

Monthly Loan Payment (principal + interest + taxes + insurance)

DSCR Ratio = Monthly Rent ÷ Monthly Payment

Sample Calculation

Monthly Rent $2,000

Mortgage + Expenses $1,600

DSCR1.25 ($2,000 ÷ $1,600)

In this example, the DSCR is 1.25, meaning the property earns 25% more than it costs to own—typically a very strong approval signal.

We only require a DSCR of 1.0 or higher, which means the property must at least break even. Some may allow lower DSCRs (0.75–0.99) with compensating factors like larger down payments or higher reserves.

Who Qualifies for DSCR Loans?

DSCR loans are built for real estate investors who meet the following:

Purchasing or refinancing an investment property

Property must generate income (long-term or short-term rentals)

Minimum credit score typically 620–660

Down payment starting at 20–25%

DSCR ratio ≥ 1.0 (some exceptions allowed)

Canadian and other countries investors welcome.

Common Scenarios Where DSCR Loans Work Best

✅ Self-employed with complex tax returns

✅ Own multiple investment properties

✅ Want to avoid traditional income documentation

✅ Using rental income from Airbnb or VRBO

✅ Need fast, flexible closing for time-sensitive deals

Start Your Investment Property Loan Today

Whether you're purchasing your first rental or expanding your portfolio, DSCR investment property loans can help you unlock more opportunities with less paperwork and faster approvals.

Contact us now to get a custom quote or pre-qualify for a DSCR loan. Take the next step toward building wealth through real estate investing.

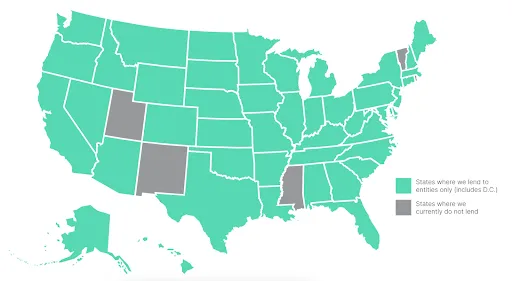

Where we lend?

Alabama, Arkansas, Colorado, Connecticut, Washington DC, Florida, Georgia, Hawaii, Illinois, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maryland, Michigan, Missouri, Montana, Nebraska, New Jersey, New Mexico, North Dakota, Ohio, Oklahoma, Pennsylvania, South Carolina, Tennessee, Texas, Virginia, West Virginia, Wisconsin, Wyoming

Frequently Asked Questions

What does DSCR stand for in real estate loans?

DSCR stands for Debt Service Coverage Ratio. It’s a measure used by lenders to determine whether a rental property's income can cover its mortgage and related expenses. A DSCR of 1.0 or higher typically qualifies.

Do I need to show tax returns or personal income for a DSCR loan?

No. One of the main advantages of a DSCR loan is that you do not need to provide personal income documentation, such as tax returns, pay stubs, or W-2s. Approval is based solely on the property’s rental income.

What is the minimum DSCR required to qualify?

Most lenders require a minimum DSCR of 1.0, meaning the property breaks even (rent = expenses). However, some lenders may accept a lower DSCR (as low as 0.75) with higher down payments or cash reserves.

What kind of properties can I finance with a DSCR loan?

DSCR loans can be used for most non-owner-occupied properties, including:

- Single-family homes

- Duplexes, triplexes, fourplexes

- Condos and townhomes

- Short-term rentals (Airbnb/VRBO)

- Multi-unit rental properties (2–4 units)

Can I use projected rent or do I need a signed lease?

We accept either a signed lease agreement or a market rent estimate provided by the appraiser (Form 1007). For vacant properties, the appraiser’s estimate is commonly used.

Are DSCR loans available for first-time investors?

Yes. Even if this is your first investment property, you can still qualify for a DSCR loan as long as the property meets the rental income and credit score requirements.